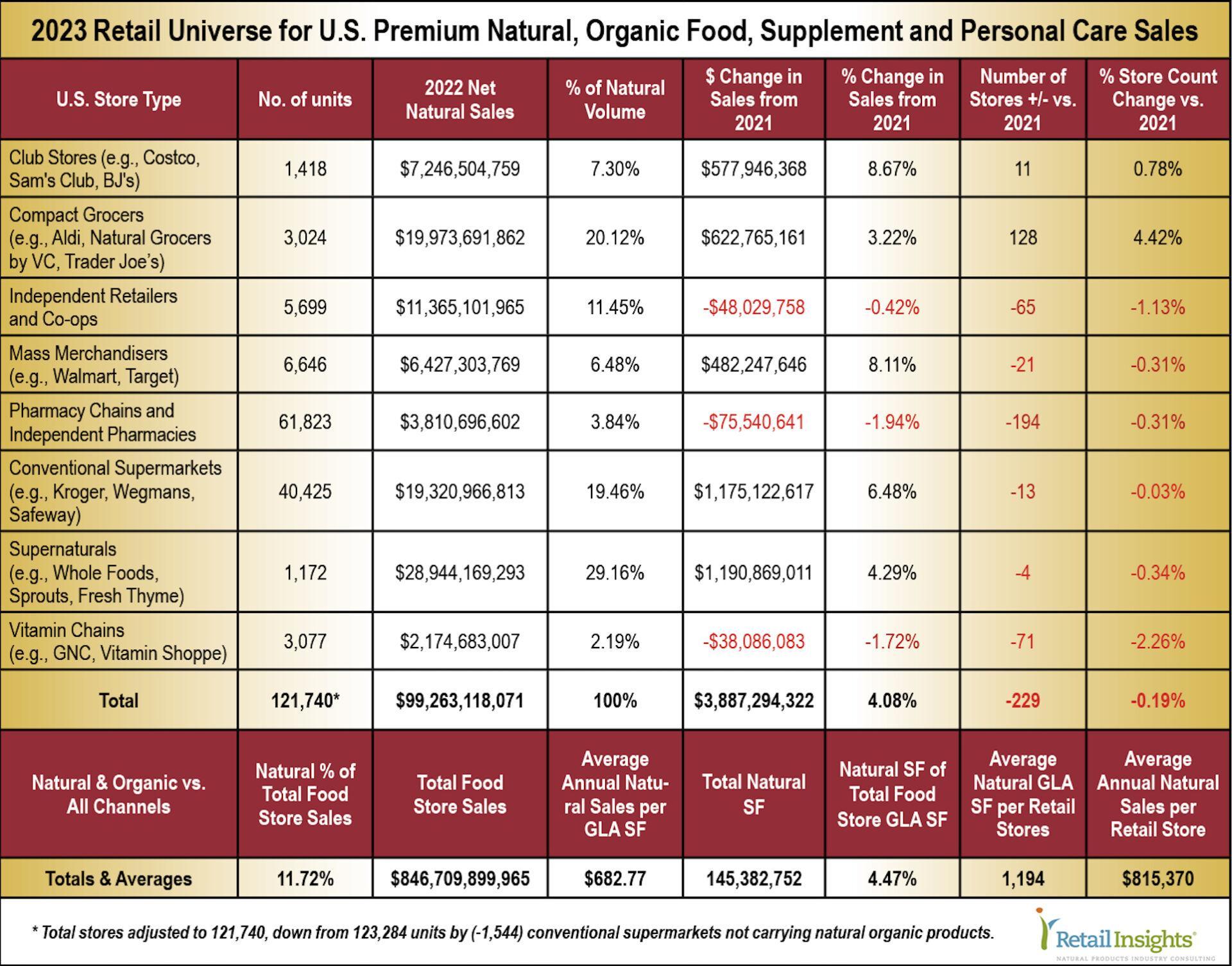

Industry grows 4.08%, adds $3.887 billion, reaches $99.3 billion total sales

Channels diverge, stores close

Club stores like Costco and mass merchandisers Walmart and Target saw the highest percentage increase in sales, up 8.67% and 8.11%, respectively. Supernaturals like Whole Foods and Sprouts, and conventional supermarkets, added the most dollars: up $1.19 billion, and up $1.175 billion, respectively. And “Compact Grocers”—those stores under 20,000 square feet like Aldi and Natural Grocers—also turned in strong results, adding $622.7 million in natural organic sales.

Three channels shed sales: pharmacy chains and independent pharmacies; independent retailers and coops; and vitamin chains GNC, The Vitamin Shoppe, and Vitamin World, losing an estimated $75.5 million, $48 million, and $38 million, respectively. Six of the eight retail channels we track reduced store counts, shedding 368 total units. These store closures were offset by Club Stores and Compact Grocers, which added 11 units and 128 units, respectively, for a net total loss of 229 store units across all eight U.S. retail channels. (Please see the table below for full industry details.)

Supernaturals lead industry growth

Supernaturals lead industry growth

Supernaturals lead industry growth

Supernaturals lead industry growth Whole Foods, Sprouts, Fresh Thyme, and other natural organic supermarkets clocked in with $1.19 billion in new sales, a 4.29% increase, retaining their industry-leading market share of 29.16%, and totaling $28.9 billion in sales. But growth this year didn’t mostly come from inside bricks-and-mortar walls. Instead, it came from Amazon Whole Foods’ online sales, which we estimate added $1.153 billion, to reach $2.69 billion fulfilled through the company’s 513 U.S. storefronts.

On their own, we believe Whole Foods’ stores have been treading water, at about $16.7 billion in 2022—not much more than the $15.6 billion we estimated in 2017 when Amazon acquired it. Sprouts tacked on $292 million to reach $6.4 billion, but Earthfare and Fairway shut three stores, and one store, respectively, shrinking an estimated $89.4 million combined. Sprouts also shut four stores, as part of its repositioning as a smaller natural organic specialist, averaging 23,000 square feet, down from 28,000 square feet under previous management. Sprouts is now focusing more on health-interested and food-curious shoppers, and less on trying to attract all consumers with indiscriminate, scatter-shot discounts. Overall, the supernatural channel trimmed four stores, to total 1,172 units this year compared to 1,176 last year.

In recent remarks, Whole Foods’ new CEO, appointed last September, Jason Buechel, made the case for the company to open smaller stores, and stores in lower-population-density areas than typical of Whole Foods’ premium big-city locations. Buechel pointed to Ideal Market, Denver, as a prototype of the small footprint the company will pursue; 22,000 square feet by our estimate. And, in Bozeman, MT, Whole Foods’ first store in that state will be 31,718 square feet, serving this low-population-density area, and drawing from a much larger geographic area than its big-city stores need to.

Buechel claims Whole Foods has a long runway for new store openings, they just won’t be in the big metro areas, and they will include smaller footprints more typical of Sprouts and Natural Grocers. It can’t feel good, if you’re Sprouts, knowing that you’ll be competing for leases with Amazon. Speaking of Amazon, the company has recently paused its new store openings under the Amazon Fresh banner. The company had quickly rolled out about 44 of these semi-conventional supermarkets, but sales results have reportedly been disappointing. In a recent interview, Amazon CEO Andy Jassy explained, “We’re experimenting with selection, checkout formats, assortment, price points.”

Compact Grocers—a durable business model

It was in 2012 when Retail Insights® first identified this new class of grocery store: under 20,000 square feet and specializing in premium food offerings. Back then, the category consisted of Natural Grocers, Trader Joe’s, and a few others. Since then, we’ve added Aldi, as the German company cleverly upgraded its assortment to include many more natural and organic items—almost exclusively under its private label brands.

The Compact Grocer channel grabs the number two natural market-share position of 20.12%, with $19.97 billion in sales, up 3.22% and $622.7 million. Store counts increased by 128 units, the bulk of which were Aldi’s 118 new stores, followed by Trader Joe’s eight new units, and Natural Grocers’ two new stores. Altogether, Compact Grocers added 4.42% to its store count, cresting 3,024 total units.

Conventional Supermarkets—right place, right time

Perhaps more than any other channel, conventional supermarkets were ideally positioned to take advantage of the surge in food inflation, and the desire of consumers to protect their health by increasing good-for-you foods, largely defined by natural and organic ingredients. Conventionals added $1.175 billion in natural organic sales, a 6.48% increase, to reach $19.3 billion in sales, claiming its third-place, 19.46% natural market share.

Overall, conventional supermarkets’ total sales—not just natural organic products—rose 8.5%, or $66.3 billion, to reach our estimate of $846.7 billion. The growth is a combination of food inflation, which ran in the low double digits throughout 2022, and our periodic adjustments to channel sales and store counts. Please keep in mind, when we cite the 11.72% in 2022 “natural organic market share” of total food-store sales, the number we use as the benchmark is the $846.7 billion generated by the conventional grocery retail channel.

Independents and co-ops

In a trend we’ve tracked over the last several years, the independent natural retail channel continues to gradually shed stores, decreasing by 65 units in 2022, to 5,699 stores, down from 5,754 in 2021, a decrease of 0.42%. Nevertheless, the surviving stores registered modest growth, which we estimate at a 0.68% increase. This modest increase muted the decrease in total sales, which drifted lower by $48 million, to reach $11.36 billion, retaining the channel’s fourth-place, 11.45% natural market share. (Please see WholeFoods Magazine’s 45th Annual Retailer Survey for a full accounting of the independent natural organic retail segment.)

Club Stores—penetrating natural organic

The big-box club stores, such as Costco, Sam’s Club and BJ’s Warehouse, tacked on the largest percentage increase in natural sales of all eight retail channels we track: adding 8.67% and reaching $7.2 billion, securing a fifth-place 7.3% natural market share. Club channel unit counts rose by 11 stores, to 1,418 in 2022 from 1,407 in 2021, a 0.78% increase.

In its quarterly conference calls, Costco continues to cite traction in fresh perishables foods, driven by premium natural and organic ingredients. By far, Costco’s estimated $553.7 million in new natural organic sales contributed the lion’s share of the club-channel’s $577.9 million natural organic growth in 2022.

Mass Merchandisers— inflation beneficiaries

The big-box mass retailers Walmart and Target also enjoyed a “right-place, right-time” benefit from consumers seeking shelter from rising food prices. Both retailers benefited from their omni-channel approach; supporting online ordering for pickup curbside, and delivery-to-home for households requiring convenience above all. Target says 20% of its sales now initiate online, 95% of which are fulfilled by its stores, rather than by separate warehouses, as many other retailers must do.

Even though the channel shed 21 units, the remaining 6,646 stores contributed to its 8.11% year-over-year growth of $482.2 million, to reach $6.4 billion in natural organic sales. This was good enough for a sixth-place 6.48% natural market share. Mass channel natural growth was shared nearly equally between the two; Walmart by virtue of its estimated 3,570 supercenters and 799 smaller neighborhood markets.

Target raised natural organic grocery sales by improving the ingredient-quality of its private label food offerings, sold mostly through its 1,515 “expanded food assortment” large-box stores. While traditionally far behind Walmart’s 56% in groceries as a percentage of sales, Target’s recent focus on increasing perishables and raising the quality of its packaged foods ingredients, makes the company more of a destination for households looking to fill in their weekly shopping.

Independent and Chain Pharmacies

Independent and chain pharmacies make up the largest share of the 121,740 stores we track annually in the Retail Insights’ Retail Universe, at 61,823 units in 2022, down 194 stores vs. 62,017 in 2021. The shrinking footprint drove a $75.5 million decline in estimated natural organic sales, to reach $3.8 billion, and a seventh-place 3.84% natural market share.

All major pharmacy chains closed stores, with CVS reducing store count by 246 units; Walgreen by 138 units, and Rite Aid with and without a GNC Live Well franchise inside, down 149 units. Offsetting this corporate chain unit loss, independent pharmacies increased their numbers by 339 stores. While this may seem surprising, the aging of the population, with its increasing need for convenient access to pharmacy services, appears to be driving independent pharmacy unit growth.

Vitamin Chains

As we’ve seen during the past decade, vitamin chain stores have continued to struggle to find traction with shoppers. The channel lost 71 units in 2022, accounting for a $38 million decrease in natural organic sales, to $2.17 billion, and an eighth-place 2.19% natural market share. Most of the store closings came from an estimated 37 corporate GNCs, 12 GNC franchisees, and 33 shuttered Vitamin Shoppes. Vitamin World closed a single unit.

While the bricks-and-mortar stores of GNC and The Vitamin Shoppe continued to lose sales, these losses were partially offset by the companies’ online e-commerce offerings, which we estimate at $223 million for GNC, and $85 million for The Vitamin Shoppe.

Natural Organic—$3.887 billion in new sales

The three retail channels we track that lost sales in 2022—independent and chain pharmacies, down $75.5 million; independent natural products retailers and co-ops, down $48 million; and vitamin chains, down $38 million—did not make a significant dent in natural organic growth in 2022. Overall, natural organic retail sales rose by $3.887 billion, led by the $1.19 billion supernaturals added, and by the $1.175 billion increase through the conventional supermarket channel.

Compact grocers—those stores under 20,000 square feet—raised a robust $622.7 million, followed by the resilient club-store channel, which grew by $577.9 million. Even mass merchandisers Walmart and Target were well positioned during inflationary times to benefit from shoppers seeking value, but also desiring healthy foods. These big-box retailers gained $482.2 million in natural organic sales in 2022.

Overall, our industry grew 4.08%, to reach $99.263 billion, which accounted for 11.72% of total food-store sales. As we noted earlier, we consider the conventional supermarket’s channel estimated $846.7 billion in total sales as the benchmark against which we measure natural organic market share.

Average annual natural sales per gross-lease-area square foot, across all 121,740 stores in our database, reached a new record of $682.77, handily beating the estimated $494.89 total food-store sales per square foot through the conventional supermarket channel.

Natural organic foods are more efficient per-square-foot—and more profitable—than conventional grocery stores. The 145.3 million total natural square feet in our model make up just 4.47% of the 3.255 billion gross-lease-area square feet we are tracking through all eight U.S. retail food-store channels. Looked at another way, $1 of natural sales requires about 62% less square footage than $1 in conventional food sales.

Summing up

It was in the early 1980s our industry reached its first $1 billion in sales. Forty years later, we are about to—and probably already have—leap over the $100 billion mark. Our nearly 12% market share of total food-store sales has remained constant over the decade we’ve tracked it. And natural organic products appear set to increase market share as households—driven by 20-something Gen Zs, and teens and youngsters in Gen Alpha—increasingly prefer and demand higher-quality foods.

Of course, nearest and dearest to our hearts at Retail Insights and at WholeFoods Magazine are the independent natural products retailers who launched this industry, and who continue strong today. For it is the independent entrepreneurs who believe deeply in natural organic products, and insist on the highest quality from manufacturers and brands, acting as the industry’s conscience. Amen! JJ

The post Retail Insights® 2023 Retail Universe for U.S. Premium Natural Organic Food, Supplement & Personal Care Sales appeared first on WholeFoods Magazine.

This content was originally published here.